Now more than ever, software development is at the core of the Insurance industry

In the coming years, the Nordic Insurance industry will face competition similar to what Banking is facing today. How should Nordic Insurers respond?

In the coming years, the Nordic Insurance industry will face competition similar to what Banking is facing today. How should Nordic Insurers respond?

Digital intermediaries will make it easier for the customer to compare insurances and chose a mix of insurances that best fit the individual customers’ needs, regardless of insurance provider. We can call it “disaggregation of insurance offerings”. Incentives for customers to stick with one insurance provider will diminish, as will the switching costs - caused by the increase in transparency and mobility between providers' offerings. These kind of startups have so far mostly showed up in banking, in the form of Tink and Opti, but are bound to impact insurance as well, sooner or later.

Completely new entrants like Lemonade will take novel approaches to insurance and claims handling, unencumbered by legacy technology, processes and thinking, taking profitable chunks of the insurance market. As late as November 2018, Lemonade announced its plans to expand to Europe. In the Nordics, Klarna is a good example that grew out of invoicing and payments but recently (2017) acquired a broader banking license and is moving into other product areas.

At the same time, capital is reasonably “cheap” and the Nordic market has higher profitability than most other regions. Re-insurers and global insurers therefore likely consider the Nordic direct insurance market to be attractive, albeit somewhat challenging to enter. But in cooperation with the startups those entry barriers will decrease; a good example of this is Hedvig – a Swedish company similar to Lemonade. And being a pure “risk carrier” is not inherently very profitable due to the low interest rates and high availability of cheap capital.

This means that the premium on top of risk rate that the industry can charge for insurances need to be justified by superior service. Insurers need to provide their customers with better service and better offerings than their (new and old) competitors in order to win in the increasingly competitive market.

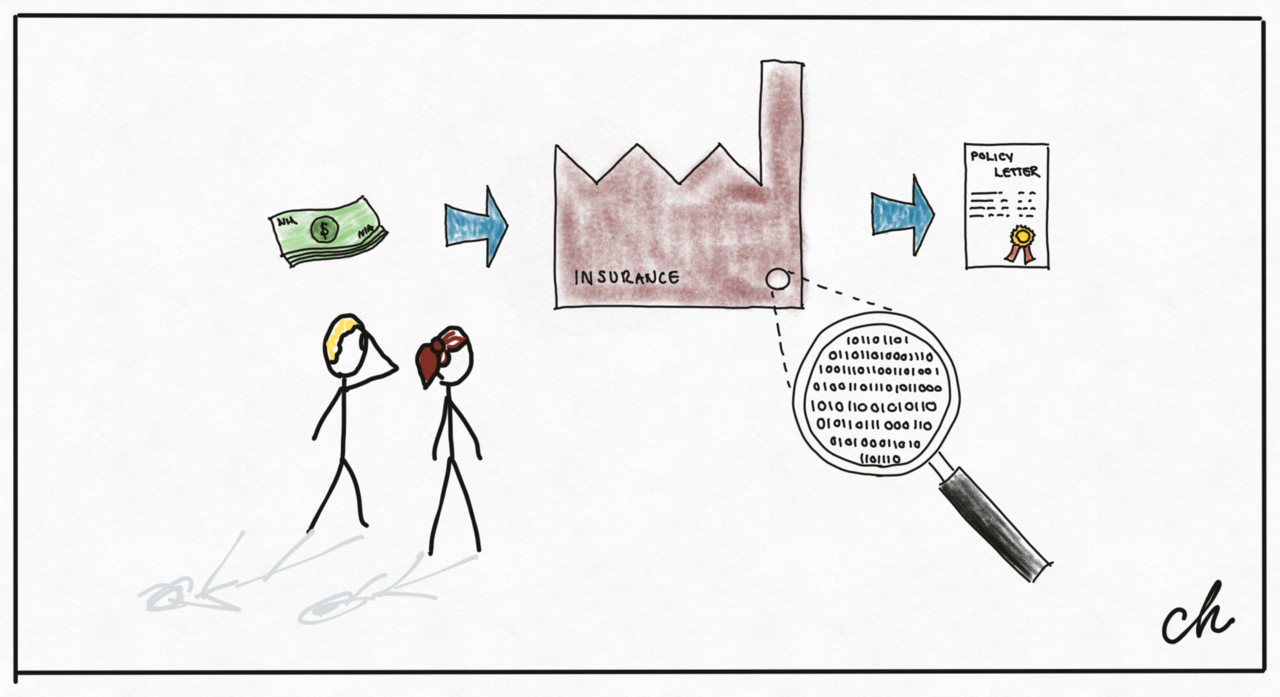

Insurance is an intangible product. The consequence is that IT becomes core business

Insurance is a product that is produced and consumed digitally. Virtually no products or processes can be changed without changing the underlying technology.

Furthermore, customers increasingly turn to digital channels to buy insurance and handle their claims. The usage of the IT solutions in Insurance is shifting from their contact center employees to end customers.

This means that it is no longer possible to "smooth over" technology problems in the contact centers and provide superior service without having superior IT solutions. Consequently, in order for insurers to differentiate from their competitors, they need to have the best technology delivery, especially in areas that matter to their customers.

Having a superior IT delivery capability is instrumental for insurers to maintain competitive advantage

Being an insurer, it is unlikely that your IT delivery capability will be consistently better than that of your competitors' - if it works identically to theirs. How can you expect your sausages to differ from those made by your competitors, if they are made in the same factory, with the same production line setup, and the same ingredients?

Instead, insurers should aim to become highly professional technology companies. Moving from being an insurance company towards becoming an "insurtech". For the Nordic insurer, this should translate into the following objectives for their technology delivery organizations:

- Aim for higher developer productivity than your competitors. You need to make sure that every developer hour that goes in, results in the largest improvement to the customer offering. This requires a bit of creative destruction in your current processes and thinking about how to empower the developers and make their life as easy as possible, while finding new ways to manage risk.

- Aim for faster cycle times than your competitors from idea to production. Don't place a big bet on an offering that will be irrelevant by the time it is launched (if it ever was). Instead build, measure, learn, improve and iterate.

- Eliminate wasteful work in the business that does not add customer / business value. There is a lot of "busy work" out there. Work that serves no purpose for the customer or business, but is done anyway, like a self-playing piano.

- Maintain an appropriate level of risk – you don’t win by gambling or making "big bets". You win by being adaptable to changes, not by making the best guess on what will happen five years ahead in time. Insurance companies tend to be risk averse, but adaptation and change inherently creates new organizational risks. The goal must be to find and navigate a path that does not create unacceptable risks, but accept that some (manageable) risks are a necessity in order to change.

The above goals are not impossible to achieve, but require new management approaches. You need to embrace the uncertainties and transform to apply methods such as Lean Startup and DevOps to foster innovation, entrepreneurship and set up the "software factory" to deliver real customer value in an uncertain and fast-paced environment.

When doing it, you also need to avoid the pitfall of expecting things to organize themselves. An enterprise-wide DevOps transformation requires a significant amount of management attention and a courage to steer and navigate the ship across the sea of organizational change.

The influx of digital startups, new entrants and global players will create an even better market for consumers. Established players need to rise to the challenge and maintain a clear focus on transforming into a professional software development company to improve their customer offerings and stay competitive in the new era.